Electricity grid “land grabs” to ensure capacity ahead of graphics processing unit (GPU) shipments. Additions to capacity as ever-larger datacentres switch on. And the arrival, deployment and “burning in” of Hopper and Blackwell GPUs.

These are some of the things we can see in data from electricity grid provider UK Power Networks (UKPN), which provides electricity utilisation rates taken half hourly for 96 datacentre sites within its region. This stretches from the datacentre hotspots of west London and Docklands, south-eastwards to Kent, Surrey and Sussex, and includes all of Essex and East Anglia.

Computer Weekly research conducted in March 2026 analysed Electricity Performance Certificate data to identify datacentre locations and capacities, finding 80 datacentres in the UKPN region with a combined capacity of 798MW.

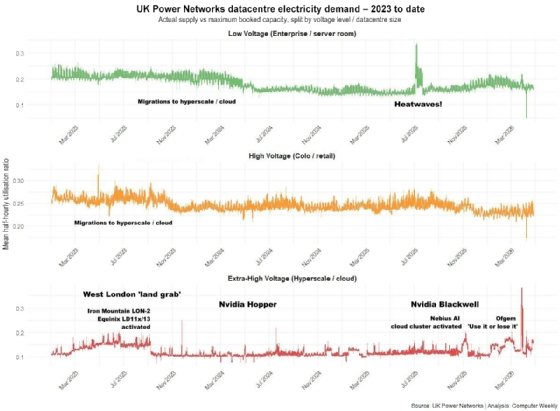

The UKPN dataset starts at the beginning of 2023 and runs to April 2026. Altogether, it comprises almost 5.4 million rows and covers datacentres categorised by the voltage they import from the grid: extra-high voltage (12 sites), high voltage (60), and low voltage (24).

Utilisation ratios are calculated by comparing actual electricity import – measured half-hourly by smart meter – against the maximum capacity booked by the customer.

Site voltage corresponds to the likely size of the datacentre. Low-voltage (LV) sites are typically 400V connections for smaller enterprises, edge datacentres and server rooms. High voltage (HV) in the UKPN data likely refers to 11kV or 33kV connections to colocation hubs and mid-range datacentres. Extra-high-voltage (EHV) connections are 33kV, 66kV, or 132kV, and cover hyperscale campuses and emerging artificial intelligence (AI) factories.

The average utilisation rate for all UKPN data is just over 20% of booked capacity. Extra-high-voltage sites use the least of their allotted supply (12%), while low-voltage sites use more (18%).

We have taken the data points and split them by voltage levels that correspond to datacentre size. These are then shown in a chart where dips, plateaus, spikes, and so on are visible. These correspond to real-world events that include activation of new datacentre capacity, increases in booked capacity in advance of AI GPU deployments, the heatwave of July and August 2025, actual deployment and “burning in” of AI datacentre infrastructure, and a rush to beat Ofgem’s “use it or lose it” directive in early 2026.

Bear in mind that the chart shows utilisation rate, so while in some cases the cause of a spike might be obvious – such as increased power draw for cooling during a heatwave – other changes might not be so obvious, such as an increase in booked capacity that changes the ratio.

Now let’s look at some of the key events that show up in the data.

Small sites can’t deal with the heatwave: July and August 2025

One of the most pronounced spikes in the green (low-voltage site) data occurred in July and August 2025, when meteorological data shows the UK faced four distinct heatwaves between June and August. Temperatures reached 35.8°C in Kent on 1 July, while August saw sustained high night-time temperatures.

The spikes in the chart show the electrical signature of smaller air-cooled datacentres and server rooms desperately trying to keep temperatures down. Unlike large hyperscale sites that use liquid cooling, smaller sites are the most vulnerable to climate stress.

They typically rely on legacy direct expansion air-conditioning. When ambient temperatures exceed 30°C, these units draw two or three times their normal power just to maintain the status quo. Electricity utilisation ratio spikes here because total facility power skyrockets while IT load remains static, resulting in a temporary collapse of power usage effectiveness (PUE).

Capacity increases: Ratios decline – late 2023 into 2024

Much of the story revealed by the data is that of large-scale sites adding capacity, and booking more electricity supply in anticipation of deliveries and deployment of GPUs. This started to happen in late 2023 and into 2024.

The sudden drop-off in September and October 2023 for the largest datacentres – the red line – is likely the result of capacity coming online.

So, when a hyperscale site activates a new phase, its import capacity – the total power booked from the grid (the denominator) – jumps instantly. But because the IT load (the numerator) only populates as servers are physically racked and “burned in” over subsequent months, the utilisation percentage appears to crash.

At the same time, we see gradual (blue line) and more pronounced (green line) declines in late 2023 and into 2024. That’s a likely indication that larger, newer, more efficient facilities are pulling general-purpose workloads away from the older small and mid-range facilities.

CBRE’s forecast for large-scale colocation take-up in London in 2024 was forecast to hit 130MW, and as this new, efficient capacity came online, it “emptied” the less efficient sites.

The fact that the smallest datacentres (likely enterprise-owned or older retail colocation sites) took until May 2024 to settle from utilisation ratios of 0.2 to 0.15 indicates a longer migration period. Unlike the hyperscalers, which move workloads in massive, software-defined blocks, smaller organisations are more likely to be bound by physical hardware lifecycles.

Sites that activated capacity in late 2023 included:

- Iron Mountain’s LON-2, with the first phase of its eventual 27MW of capacity in Slough, was confirmed as operational at the end of 2023. Its grid capacity was likely booked into the UKPN system in September 2023 as part of its pre-commissioning phase.

- Equinix’s LD11x/LD13 expansions, meanwhile, were specifically designed to lure the big three hyperscalers, and moved from construction to “available capacity” in late 2023.

GPU supply constraint and the ‘West London land grab’

From late 2023, the lead times on Nvidia GPU clusters became very lengthy, with Omdia reporting 36 to 52 weeks for H100-based servers. At the same time, datacentre operators scrambled for grid supply, often booking way beyond what they would immediately use so they could be ready to deploy Hopper GPUs when they finally arrived in mid- to late-2024. That’s another reason grid utilisation appears to plummet in late 2023 in the chart.

In July 2022, the Greater London Authority (GLA) sent a warning to developers, stating that major new planning applications in Hillingdon, Ealing and Hounslow would face delays of up to a decade, with some connection dates pushed back as far as 2035 or 2037.

That breaking point was triggered by the extreme concentration of datacentres along the M4 corridor. By mid-2023, datacentres accounted for 18% of total demand in West London. Transmission-level capacity and local distribution reached full capacity because developers had legally “reserved” future power capacity and left zero headroom for new housing or industrial projects.

Financial reports from datacentre Real Estate Investment Trusts (REITs) like Equinix and Digital Realty back this up. In their 2023 annual reports, these firms noted record “backlog” levels, where capacity was signed and committed but not yet billing.

In the data, a high backlog means the distribution network operator (UKPN) has allocated the power, but the servers aren’t spinning, and this matches the 2023-2024 trough where utilisation ratios settled at a lower baseline compared with the pre-AI land grab.

The reason the ratio didn’t bounce back immediately is that AI density is more efficient than legacy density. A rack of H100s might draw 40kW, but it replaces dozens of legacy racks drawing 5kW each. As hopper GPUs finally arrived in mid- to late-2024, they filled that phantom capacity, but because grid capacity had been aggressively over-booked in 2023, utilisation ratios remained low. The industry effectively built a buffer that it is still filling today.

GPU deployment, AI datacentre burn-in: 2024 and 2025

The peaks of mid-2024 fit with the likely deployment of Nvidia Hopper (H100/H200) GPUs. The Hopper generation was the first GPU to hit a 700W Thermal Design Power (TDP) – ie, the wattage for which its cooling had to be designed. An HGX H100 node of eight GPUs draws roughly 10.2kW. The spikes in the data from late-2024 likely represent the initiation of large-scale training runs where thousands of these units synchronise their power draw.

These represented a shift in datacentre power dynamics, from the steady-state draws of the previous Ampere (A100) generation to highly volatile, high-density profiles.

Late 2025 marked a pivot from Hopper to Blackwell’s high-density liquid-cooled requirements. This transition is reflected in the UKPN telemetry as a distinct shift from steady-state power draw to the volatile, “peaky” plateaus of large-scale Blackwell training epochs.

The “mountain range” in the chart beginning in November 2025 marks the power-on month for the UK’s first Nvidia Blackwell (B200) clusters. This is the signature of initial model training, which is an extremely intensive, non-stop process.

Each B200 GPU has a base 1,000W TDP, configurable up to 1,200W. The GB200 Grace-Blackwell Superchip, meanwhile – which shipped from late 2024 – mandated direct-to-chip liquid cooling to manage its extreme density.

The smoking gun here is the launch of the Nebius AI Cloud cluster at Ark Data Centres’ Longcross Park in Surrey. This went live in November 2025 with several thousand Nvidia Blackwell GPUs and a 16MW signature.

The EHV line remains elevated and jagged through March 2026, reflecting the high, sustained draw of “epochs” and “checkpoints” during frontier model pre-training.

One final spike: Use it so they don’t lose it?

The giant spike in late March 2026 coincides with the Ofgem Demand Connections Reform deadline of 13 March 2026.

In the face of massive increases in electricity demand, not least by datacentre operators – and with the demand queue soaring to 125GW by June 2025 – Ofgem had proposed tougher financial tests and “use it or lose it” rules to clear the queue. Large-scale operators with parked capacity were incentivised to show power draw to prove their projects were “viable” and “strategically important” before the new rules could claw back their unutilised megawatts.